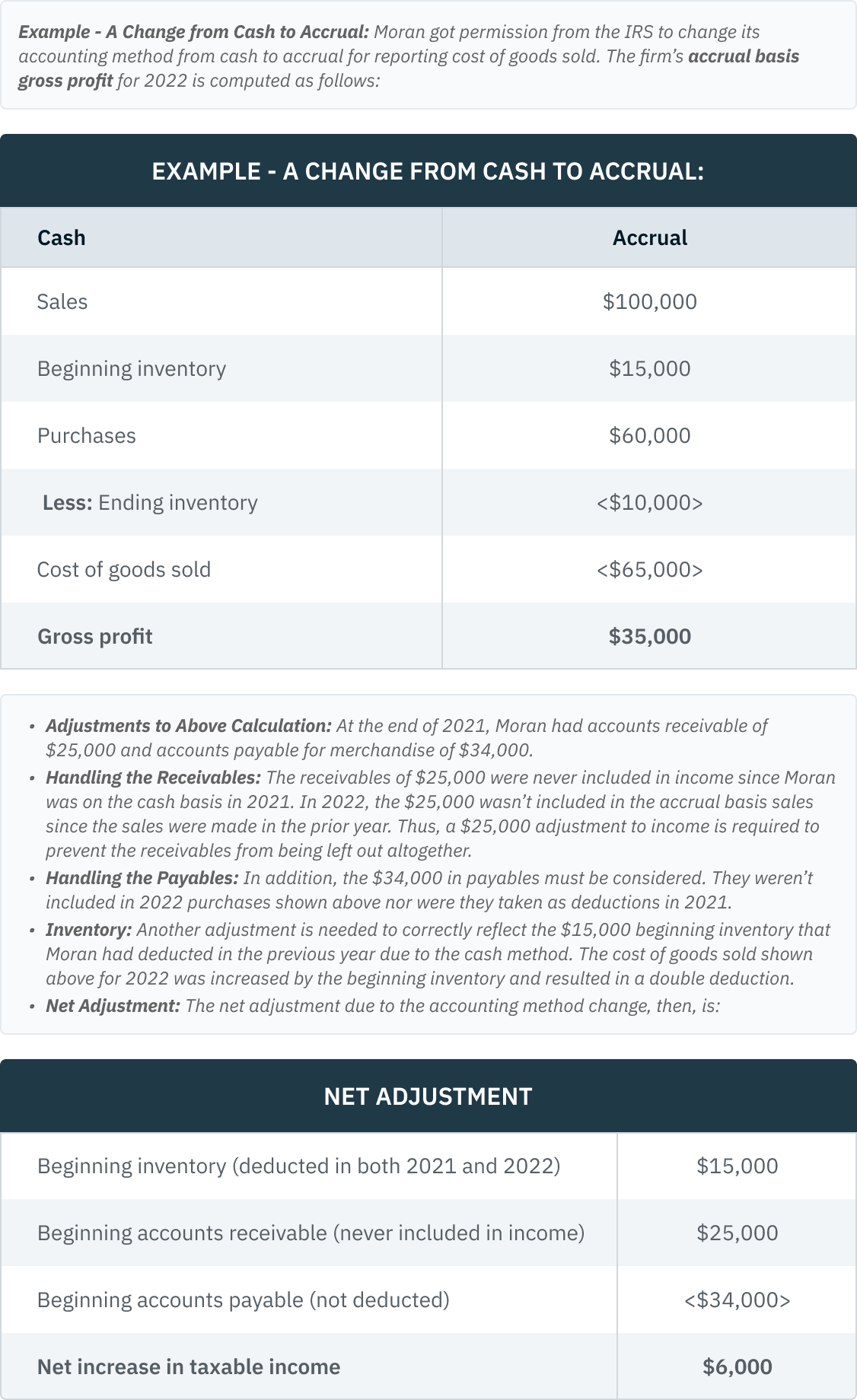

Change of Accounting Method

It is important for business owners to understand that it is not always easy to change accounting methods once one has been selected. While a switch can be made, the process is often complex. Due to this, it is wise to engage assistance from a tax professional to choose the best accounting method for you during your company's first year in business.

A taxpayer’s choice of accounting method on his/her first tax return controls the accounting method to be used in future years. To change an accounting method, IRS consent is needed. File Form 3115, Application for Change in Accounting Method, to obtain consent. Unless the change is “automatic” (see below), as of February 4, 2021, a user fee of $11,500 (up from $10,800 for requests received 2/2/2020 through 2/3/2021) applies. A reduced fee of $8,500 (was $7,600) applies to taxpayers with a personal or business-related tax issue whose gross income is less than $1 million but over $250,000 or a fee of $3,000 (was $2,800) for taxpayers with a personal or business tax issue whose gross income is less than $250,000 (see Rev. Proc. 2021-4, Appendix A). These fees are subject to change annually.

Starting August 16, 2017, when requesting an accounting method change for which a user fee is required, taxpayers will only be able to make the user fee payment through the federal government’s Pay.gov system. Since Pay.gov is used only to accept payments, the original, signed request and any supporting materials must still be submitted to the IRS. This electronic payment requirement also applies to requests for letter rulings and certain other rulings. (IR 2017-102) Pay.gov accepts payments using a credit card, debit card, or via direct debit or electronic funds withdrawal from a checking or savings account.

The following are some considered accounting method changes that require IRS approval:

-

A change from accrual to cash if not an eligible small business taxpayer;

-

A change in the method of basis used to value inventory;

-

A change in the method of figuring depreciation (other than permitted changes to straight-line for property placed in service before 1981).

On the other hand, these changes don’t require any approval:

-

A change from cash to accrual, or for eligible small business taxpayers, from accrual to cash;

-

Corrections of math or posting;

-

Corrections of errors in computing tax liability;

-

Adjustments to income or deductions that involve timing of inclusion or deduction;

-

Adjustments to the useful life (not the recovery period of ACRS or MACRS assets) of depreciable property.

NOTE

Accounting changes related to tangible property capitalization and repairs are covered in Chapter 3.27.

Automatic Change Procedures

The automatic change procedures were instigated to simplify and encourage compliance to IRS guidelines. The automatic change procedures may apply to changes in the following:

-

Trade and business expenses;

-

Depreciation or amortization (including changing impermissible depreciation methods);

-

Research and experimental expenses;

-

Capital expenses;

-

UNICAP rules;

-

Plan contributions and deferred compensation under Code Section 404;

-

Method of accounting;

-

Discount obligations (bonds, etc.);

-

Prepaid subscription income;

-

Inventories;

-

LIFO issues.

For a complete list of accounting method changes to which the automatic change procedures apply see Rev. Proc. 201831, modified by Rev. Proc. 2018-35 (related to certain costs for replanting citrus plants after the loss or damage of citrus plants), Rev. Proc. 2018-40 (relates to small business taxpayers changing to overall cash method), Rev. Proc. 2018-44 (concerns the Sec 481(a) adjustment), Rev. Proc. 2018-49 (modifies Rev Procs 2018-31 and 2018-29), Rev. Proc. 201856 (modifies Rev. Proc. 2018-31 to provide additional automatic method changes under §1.263A-1, -2, and -3 to assist taxpayers in complying with the final regulations), Rev. Proc. 2018-60 (modifies Rev Proc 2018-61 related to the timing of income recognition under §451(b) for a taxpayer with an applicable financial statement (AFS)) and Rev. Proc. 2019-37 (relates to automatic consent to comply with proposed regulations re AFS). Other pertinent revenue procedures include Rev. Proc. 2019-8 (relates to the election out of the business interest limitation and use of ADS depreciation) and Rev. Proc. 2019-33 (modified by Rev Proce 2020-50 and relates to bonus depreciation for tax years that include Sept. 28, 2017). Further, Rev Proc 2019-43 provides updates to the List of Automatic Changes to which the automatic change procedures apply.

Also see Rev Proc 2022-14 (which modifies the following Rev. Procs.: 2004-34, 2011-18, 2013-26, and 2013-39) for a listing of the specific changes in accounting method to which the automatic change procedures set forth in Rev. Proc. 2015-13 apply. This guidance updates and supersedes the list of automatic changes found in Rev. Proc. 2019-43. Rev

Proc 2022-14 is effective for a Form 3115 filed on or after January 31, 2022, for a year of change ending on or after May 31, 2021, that is filed under the automatic change procedures. This revenue procedure is over 450 pages and can be accessed here: RP-2022-14 (irs.gov)

Filing Form 3115

Individuals, partnerships, corporations (C and S), personal service corporations, cooperatives, insurance companies, controlled foreign corporations, estates and trusts, and tax-exempt organizations use this form to request an accounting method change. If the change is one for which automatic consent is granted, the completed Form 3115 must be filed in duplicate, and by the due date (including extensions) for the return for the year of the change. The original 3115 is attached to the taxpayer’s return, and a signed copy of the application must be filed with the IRS in Ogden, UT no earlier than the first day of the year of the change (and no later than the filing of the original with the return). The mailing address is included in the 3115 instructions, available at: https://www.irs.gov/pub/irs-pdf/i3115.pdf. The IRS does not send acknowledgements of receipt for automatic change requests.

Non-Automatic Change Requests

For non-automatic change requests Form 3115 must be filed during the tax year for which the change is requested, unless otherwise provided by published guidance. (See Rev. Proc. 2015-13, section 6.03(2)). Form 3115 is filed with the IRS National Office at the address listed in the address chart in the 3115 instructions. The Form 3115 should be filed as early as possible during the year of change to provide adequate time for the IRS to respond prior to the due date of the taxpayer’s return for the year of change. The IRS normally sends an acknowledgment of receipt within 60 days after receiving a Form 3115 filed under the non-automatic change procedures.

Extensions

No extensions for filing Form 3115 are granted unless for very unusual circumstances and an additional fee may apply. However, a taxpayer filing for an automatic change is granted an automatic extension of six months from the unextended due date of the return for the year of change if the taxpayer: (1) timely filed (including extensions) its federal income tax return for the year of change, (2) files an amended return within the six-month extension period in a manner consistent with the new accounting method, (3) attaches the original application to the amended return, (4) files a copy of the application with the Ogden office no later than when the original is filed with the amended return, and (5) attaches a statement to the application that the application is being filed pursuant to Reg. §301.9100-2. (Rev. Proc. 2015-13, 6.03(4)(a)).

Income Adjustments

When changing an accounting method under the various revenue procedures noted above, an income adjustment is required under IRC Sec 481. This adjustment must be made to account for changes in taxable income due to the change. The adjustment is made over 4 tax years beginning with the year of the change. However, a taxpayer can elect to account for an adjustment in one year if the total is less than $50,000 (Rev Proc 2015-13). It is probably best for taxpayers to accelerate negative adjustments of less than $50,000 into one year and use the 4-year period for positive adjustments. There are no different adjustment periods for different categories of accounting method changes.