1041 Income

Trust and estate income generally has the same character and is treated the same as individual 1040 income, in fact as noted, 1040 schedules are frequently used to report trust business income.

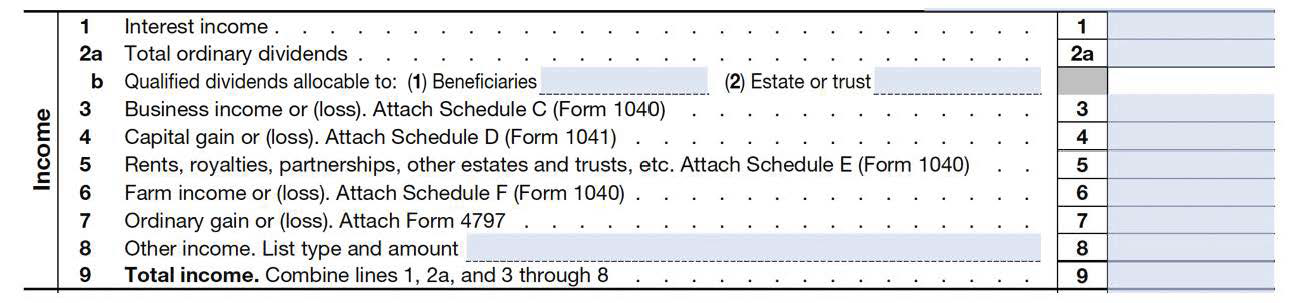

Line 1

Report the estate's or trust's share of all taxable interest income that was received during the tax year.

-

Year of Death – Include any interest reported on the decedent’s 1099(s) that is post-death interest. On the decedent’s 1040 show the entire amount on the Schedule B (to match the 1099(s)). Below the subtotal, enter “Form 1041” and the name and address shown on Form 1041 for the decedent's estate, show the part of the interest reported on Form 1041 and subtract it from the subtotal.

Line 2a

Report the estate's or trust's share of all ordinary dividends received during the tax year. For the year of the death make the same adjustment as indicated for Line 1.

Line 2b

Enter the beneficiary's allocable share of qualified dividends on line 2b(1) and enter the estate's or trust's allocable share on line 2b(2).

If the estate or trust received qualified dividends that were derived from income in respect of a decedent (IRD), the amount on line 2b(2) must be reduced by the portion of the estate tax deduction claimed on Form 1041, page 1, line 19, that is attributable to those qualified dividends. Don't reduce the amounts on line 2b by any other allocable expenses.

Note: The beneficiary's share (as figured above) may differ from the amount entered on line 2b of Schedule K-1 (Form 1041).

Line 3 - Business Income or (Loss)

If the estate operated a business, report the income and expenses on Schedule C (Form 1040), Profit or Loss from Business. Enter the net profit or (loss) from Schedule C on line 3.

Line 4 - Capital Gain or (Loss)

Enter the gain from Schedule D (Form 1041), Part III, line 19, column (3), or the loss from Part IV, line 20.

If a capital gain was deferred into a Qualified Opportunity Fund (QOF), the return must be filed with Schedule D, Form 8949, and Form 8997 attached. Form 8997 will need to be filed annually until the investment is disposed of. See the Form 8997 instructions.

Line 5 - Rents, Royalties, Partnerships, Other Estates and Trusts, etc.

Use Schedule E (Form 1040), Supplemental Income and Loss, to report the estate's or trust's share of income or (losses) from rents, royalties, partnerships, S corporations, other estates and trusts, and REMICs. Also use Schedule E (Form 1040) to report farm rental income and expenses based on crops or livestock produced by a tenant. Don't use Form 4835. Enter the net profit or (loss) from Schedule E on line 5.

If the estate or trust received a Schedule K-1 from a partnership, S corporation, or other flow-through entity, use the corresponding lines on Form 1041 to report the interest, dividends, capital gains, etc., from the flow-through entity.

Line 6 - Farm Income or (Loss)

If the estate or trust operated a farm, use Schedule F (Form 1040), Profit or Loss from Farming, to report farm income and expenses. Enter the net profit or (loss) from Schedule F on line 6.

Line 7 - Ordinary Gain or (Loss)

Enter from line 17, Form 4797, Sales of Business Property, the ordinary gain or loss from the sale or exchange of property other than capital assets and from involuntary conversions (other than casualty or theft).

Line 8 - Other Income

Enter other items of income not included on lines 1, 2a, and 3 through 7. List the type and amount on an attached schedule if the estate or trust has more than one item. Items to be reported on line 8 include the following:

-

Unpaid compensation received by the decedent's estate that is IRD.

-

Any part of a total distribution shown on Form 1099-R, Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., that is treated as ordinary income.

-

Taxable contributions received during the tax year by an Alaska Native Settlement Trust from an Alaska Native Corporation. Report gains from taxable contributions of noncash property on Schedule D (Form 1041).