Computing the Credit Phase-out

The full credit is only available to ESEs with 10 or fewer full-time equivalent employees (FTEs) with an average annual full-time equivalent wage (AAEW) of $25,000 (adjusted for inflation and shown in the table above) or less. If either or both of these thresholds are exceeded, then the credit is reduced.

There is no credit reduction if there are 10 or fewer FTEs with an AAEW of $28,700 (2022) or less.

There is no credit if the FTEs exceed 25 or the AAEW exceeds $57,400 (2022).

To figure the reduction of credit when the limits are exceeded, the number of the employer’s full-time equivalent employees (FTE’s) and average annual full-time equivalent wages (AAEW) for the year must be determined.

Figuring the Number of FTEs

An employer’s FTEs is determined by dividing the total hours the employer pays wages during the year (but not more than 2,080 hours per employee) by 2,080. (Code Sec. 45R(d)(2)) The result, if not a whole number, is then rounded down to the next lowest whole number if any. However, if the resulting number is less than one, round up to one FTE. (Reg. 1.45R-2€) Also see “Excluded Employees” below.

An employee’s hours of service for a year include each hour for which an employee is paid, or entitled to payment, for (a) the performance of duties for the employer; and (b) for vacation, holiday, illness, incapacity (including disability), layoff, jury duty, military duty or leave of absence (except that no more than 160 hours of service are required to be counted for an employee on account of any single continuous period during which the employee performs no duties). (Notice 2010-44, Sec. II.C.) (Reg. 1.45R-2(d)(1))

In calculating the total number of hours of service that must be taken into account for an employee for the year, the employer may use any of three methods:

-

Determine actual hours of service from records of hours worked and hours for which payment is made or due (payment is made or due for vacation, holiday, illness, incapacity, etc.);

-

Use a days-worked equivalency where the employee is credited with 8 hours of service for each day for which he would be required to be credited with at least one hour of service under (1), above; or

-

Use a weeks-worked equivalency where the employee is credited with 40 hours of service for each week for which he would be required to be credited with at least one hour of service under (1), above. (Notice 201044, Sec. II.C.) (Reg. 1.45R-2(d)(2))

Calculating Average Annual Wages (AAEW)

Average annual wages is determined by dividing the employer’s total FICA wages (without regard to the wage base limitation) for the tax year by the number of the employer’s FTEs for the year (rounded down to the nearest $1,000) (Code Sec. 45R(d)(3)(A); Reg. 1.45R-2(f))

Credit Reduction

If the number of FTEs exceeds 10 or if AAW exceeds $30,700 (2023), the amount of the credit is reduced (but not below zero). Both reductions can apply at the same time!

FTE Reduction - If the number of FTEs exceeds 10, the reduction is determined as follows:

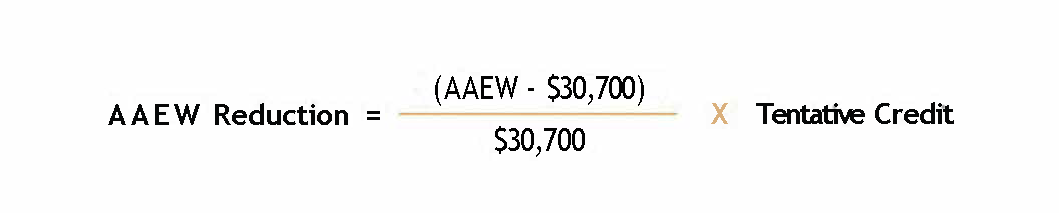

AAEW Reduction - If average annual wages exceed $30,700 (2023), the reduction is determined as follows:

Example – Joe owns a small California wood working business and has 12 employees, not counting himself or family members. The total FICA wages (without regard for wage base limitations) for 2023 were $488,000 and total hours worked by his employees during the year were 24,400. None of his employees worked more than 2,080 hours during the year. Joe made non-elective contributions to purchase health insurance for his employees in the amount of $49,800 for the year. Joe’s credit is determined as follows:

-

Small Business Benchmark Premium (estimated for this example. In actual practice the benchmark premiums are included in the instructions for Form 8941) = 12 x 6,565 = $78,780

-

Smaller of actual premium paid or Benchmark premium = $49,800

-

Tentative credit = $49,800 x 0.50 = $24,900

-

Full-time equivalent employees (FTEs) = 24,400/2080= 11.7 rounded down = 11

-

Average annual full-time equivalent wages (AAEW) = 488,000/11 = $44,3644 rounded down = $44,000

-

FTE Reduction = ((11-10)/15) x $24,900 = $1,660

-

AAEW Reduction = ((44,000-30,700)/30,700) x $24,900 = $11

-

Joe’s health insurance tax credit = $24,900 - $1,660 - $11 = $23,229

Other Issues

-

Aggregation rules apply in determining the employer. (Code Sec. 45R(b); Reg. 1-45R-2(b))

-

The credit is available for a domestic (household) employee of a sole proprietor of a business, and there's a special rule to prevent sole proprietorships from receiving the credit for the owner and their family members.(IRS Notice 2010-82) o The credit is available for tax liability under the alternative minimum tax. (Reg. 1-45R-5(b))