Computing the Excise Tax (Penalty)

For 2023 (and for employers with non-calendar-year plans, any calendar months during the 2022 plan year that fall in 2023 ), an employer that was an ALE in 2022 (had at least 50 EFTE in 2022), will be liable for an Employer Shared Responsibility payment only if:

-

The employer does not offer health coverage or offers coverage to fewer than 95% of its FTE and the dependents of those employees, and at least one of the full-time employees receives a premium tax credit to help pay for coverage on a Marketplace, OR,

-

The employer offers health coverage to at least 95% of its FTE and the dependents of those employees, but at least one full-time employee receives a premium tax credit to help pay for coverage on a Marketplace, which may occur because the employer did not offer coverage to that employee or because the coverage the employer offered that employee was either unaffordable to the employee or did not provide minimum value.

Preparer Trap

If an employer offers an employee affordable minimum essential insurance, then that employee is not eligible for a PTC and will have to repay the APTC for any month the employer offers the affordable minimum essential insurance coverage. In these cases, the employer would not be subject to the penalty. However, if an employee does obtain coverage from the Marketplace and does not tell the Marketplace that his employer offers affordable minimum essential care, the Marketplace will allow APTC and include it on the 1095-A. At the same time the employer will issue a 1095-C showing the employee was offered qualifying care, making the employee ineligible for the PTC, and thus the employee must repay any APTC received for the months the employer offered the employee affordable minimum essential insurance. This is where preparers that don’t review the 1095-C for offers of coverage may allow the PTC on the return. In which case, they will have to deal with the IRS PTC disallowance letter down the road.

ALE Offers No Coverage

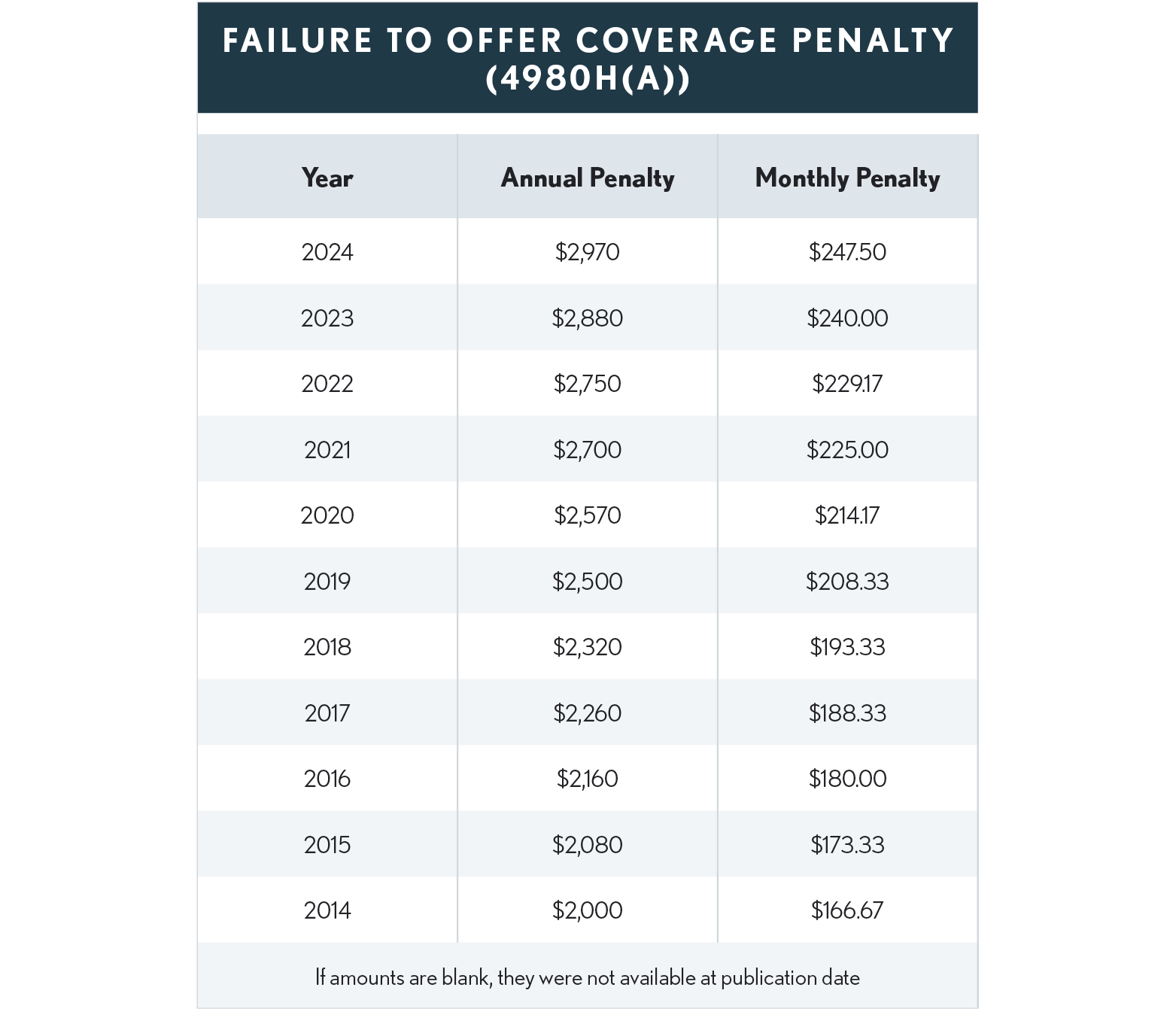

For an employer who does not offer coverage or offers it to fewer than 95% of its fulltime employees and their dependents, the excise tax penalty for any month in 2023 would be $240.00 ($2,880/12) times the number of full-time employees in excess of 30.

Employer Offers Coverage and One or More Employees Qualifies for Premium Assistance Credit

An ALE would be liable for the penalty (figured monthly) if the employer offers coverage, but the cost of the coverage is not affordable for one or more employees, or the insurance does not provide minimum (60%) coverage.

-

Offers to 95% of its full-time employees (and their dependents) the opportunity to enroll in “minimum essential coverage” under an “eligible employer-sponsored plan” for that month; and

-

At least one full-time employee has been certified to the employer as having enrolled for that month in a qualified health plan for which a premium tax credit or cost-sharing reduction is allowed or paid with respect to the employee.

The excise tax penalty for any month in 2023 would be 360.00 ($4,320/12) times the number of full-time employees that receive premium tax credit or cost-sharing reductions through an insurance Marketplace but not to exceed the penalty imposed had the employer not offered health care insurance.

Example – Health Care Plan and Employees Qualify for Premium Tax Credit or Cost Sharing Reductions – In January of 2023, an applicable large employer with 120 employees offers a health care plan to its employees, but the cost of the plan does not meet the affordable criteria (employee contribution is more than 9.12% of the employee's household income or the plan's share of the total allowed cost of benefits is less than 60%) and 20 of the employees sign up for health insurance through an insurance Marketplace and receive a Premium Tax Credit or Cost-Sharing Reductions. The employer’s excise tax penalty is $360.00 times 20. Thus, the penalty for the month of January is $7,200, which is less than the $21,600 (120-30 = 90 x $240) penalty that would apply if no coverage was offered.

-

Effect of Employees Purchasing Other Coverage

If an employer offers health coverage that is affordable and that provides minimum value to its full-time employees and their dependents, the fact that some of the employees (or their spouses or dependents) either purchase health insurance through a Marketplace or enroll in Medicare or Medicaid, won't cause the employer to be subject to an employer shared responsibility payment. Liability for that payment is triggered by a full-time employee's receipt of a premium tax credit, and an employee who is offered affordable coverage that provides minimum value is ineligible for the credit. (Q&As 21 - 23)

Minimum Value (Minimum Essential Coverage)

If an employer fails to provide health care coverage that offers a minimum value (minimum essential coverage), and as a result employees become eligible for a Code Sec. 36B premium tax credit or cost-sharing reduction (see Chapter (section) 12.02), the employees’ eligibility will, in turn, cause the employer to be subject to the penalty. Thus, knowing what minimum value means is important for both the employer and employee. The term minimum value (MV) is described in a number of ways:

-

Under Code Sec. 36B(c)(2)(C)(ii), a plan fails to provide MV if the plan's share of the total allowed costs of benefits provided under the plan (as determined under Secretary of Health and Human Services (HHS) regs) is less than 60% of the costs. In addition, to qualify as providing minimum value, employer-sponsored health plan benefits must include substantial coverage of inpatient hospital and physician services.

-

Under 36B(c)(2)(C)(i)(II), an employer-sponsored plan is not affordable if the employee's required contribution for 2023 with respect to the plan exceeds 9.12% of his household income for the tax year. For 2024 the affordability percentage is 8.39%, the lowest it has been since the ACA was enacted. (Rev Proc 2023-29) This low percentage may cause some health plans to fail to meet an affordability safe harbor and expose more employers to the IRC Section 4980H(b) penalties. When determining the applicable percentage of income, that percentage is applied to the employee’s coverage only.

Example: Carl is married to Jane, and Carl’s employer’s plan requires Carl to contribute $5,300 for coverage for Carl and Jane for 2023, which reflects 11.3% of Carl's household income. However, because the portion of the contribution ($3,750) attributable to Carl’s self-only coverage does not exceed 9.12% of Carl’s household income, Carl’s employer’s plan is considered affordable for Carl and Jane. (Reg. § 1.36B-2(c)(3)(v)(D), Example 2)

-

Proposed reliance regulations clarify the term minimum value (minimum essential coverage) and provide the following safe-harbor plans (however, as noted above, health plans which don’t offer substantial coverage for in-patient hospitalization services or physician services or both will not be considered to provide minimum value, even if they would otherwise fit into one of the safe harbors):

-

A plan with a $3,500 integrated medical and drug deductible, 80% plan cost-sharing, and a $6,000 maximum out-of-pocket limit for employee cost-sharing;

-

A plan with a $4,500 integrated medical and drug deductible, 70% plan cost-sharing, a $6,400 maximum out-of-pocket limit, and a $500 employer contribution to an HSA; and

-

A plan with a $3,500 medical deductible, $0 drug deductible, 60% plan medical expense cost-sharing, 75% plan drug cost-sharing, a $6,400 maximum out-of-pocket limit, and drug co-pays of $10/$20/$50 for the first, second and third prescription drug tiers, with 75% coinsurance for specialty drugs.

A minimum value calculator is available online at https://www.cms.gov/cciio/resources/regulations-andguidance/index.html. Enter “minimum value calculator” in the search box.

Who Computes the Employer Penalty

The employer is not required to calculate a payment with respect to Section 4980H or file returns submitting such a payment. Instead, after receiving the information returns filed by applicable large employers under Sec 6056 and the information about employees claiming the premium tax credit for any given calendar year, the Internal Revenue Service (IRS) will determine whether any of the employer’s full-time employees received the premium tax credit and, if so, whether an assessable payment under § 4980H may be due. If the IRS concludes that an employer may owe such an assessable payment, it will contact the employer, and the employer will have an opportunity to respond to the information the IRS provides before a payment is assessed. (Notice 2013-45)

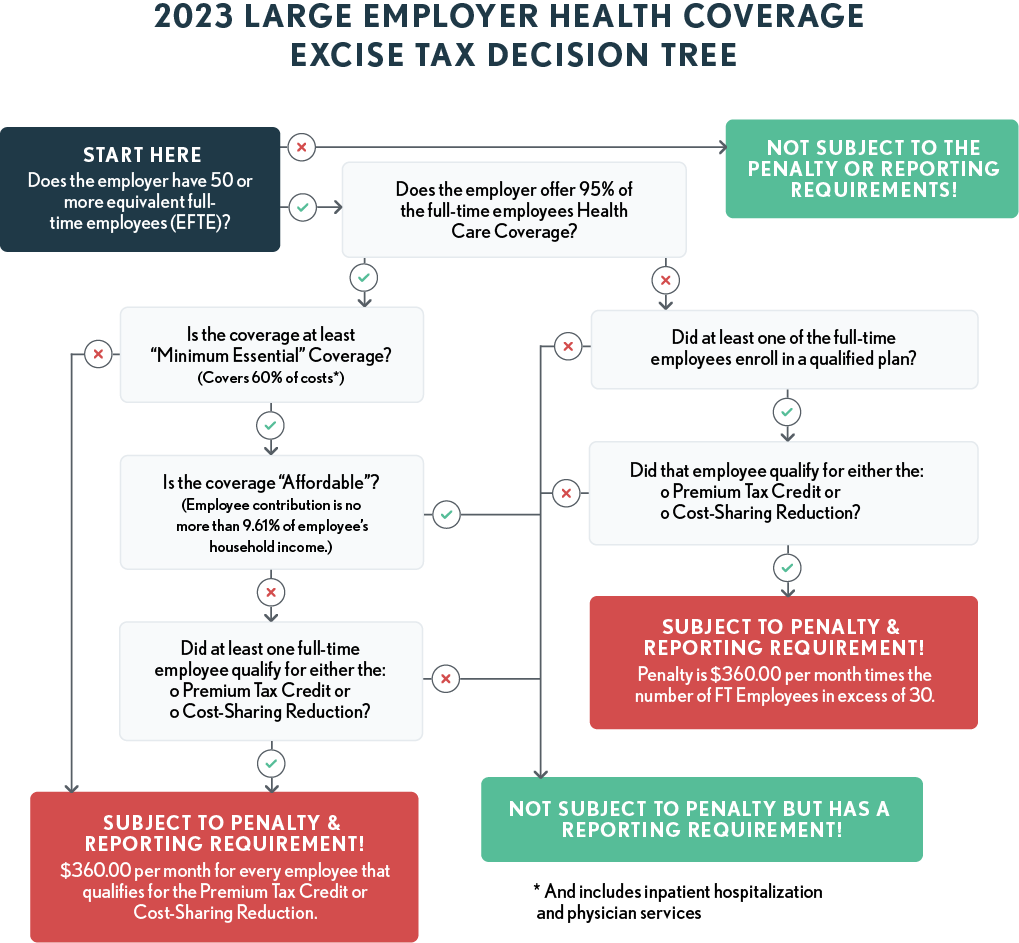

Penalty – Decision Tree

The flow chart below provides an overview of the large employer health care excise tax.

IRS Says There’s No Statute of Limitations for Assessing the Employer Shared Responsibility Payment

The Office of Chief Counsel held that there is no statute of limitations on the assessment of the Sec 4980H employer shared responsibility payment (ESRP). Since there’s no return that contains the necessary data to calculate the amount of an

ESRP that could be owed by an applicable large employer (ALE), there is no statute of limitations for the ESRP under Code Sec. 6501(a). The filing of Forms 1094-C and 1095-C is not sufficient to begin the running of the statute of limitations because they, too, do not contain sufficient data to calculate the amount of the ESRP that would be owed.

Based on numerous cases over the years, the Supreme Court’s test to determine whether a document is sufficient for statute of limitations purposes has the following elements:

-

There must be sufficient data to calculate tax liability.

-

The document must purport to be a return.

-

There must be an honest and reasonable attempt to satisfy the requirements of the tax law; and

-

The taxpayer must execute the return under penalties of perjury.

Thus, the Supreme Court test wouldn’t be met about the ESRP, and since Congress hasn’t provided any other limitations period for assessing the ESRP, there is none that is applicable. (Field Attorney Advice 20200801F)