“Affordable” Determination Safe Harbor

For 2023, the law defines affordable coverage as not costing the employee more than 9.12% (down from 9.61% in 2022) of the employee’s household income. See W-2 Safe Harbor table below for other recent years’ percentages. But how is an employer able to determine an employee’s household income? Under safe harbor rules in the final regulations, an employer can use the wages they pay, their employees' hourly rates, or the federal poverty level to determine whether the coverage is affordable. (Q&As 19 - 20)

Important Concept to Understand

An employer must offer, not provide, affordable minimum essential coverage. However, for an employer’s lower paid employees the employer may have to pay part of the premium to make the insurance affordable.

Rate of Pay Safe Harbor

-

Hourly Employee – The safe harbor for 2023, is satisfied for a calendar month if the employee’s required contribution does not exceed 9.61% of an amount equal to 130 multiplied by the employee's hourly rate of pay as of the first day of the coverage period, generally the first day of the plan year.

-

Salaried Employee – The safe harbor for 2023 is met if the employee’s required contribution for the month does not exceed 9.12% of the employee's monthly salary as of the first day of the coverage period, generally the first day of the plan year. The employer is permitted to use any reasonable method for converting payroll periods to monthly salary.

Federal Poverty Line Safe Harbor

-

All Employees – To meet the safe harbor under this method, the employee’s contribution must not exceed 9.12% of a monthly amount determined as the “Federal poverty line” (see poverty table under Premium Assistance Credit) for a single individual for the applicable calendar year, divided by 12.,

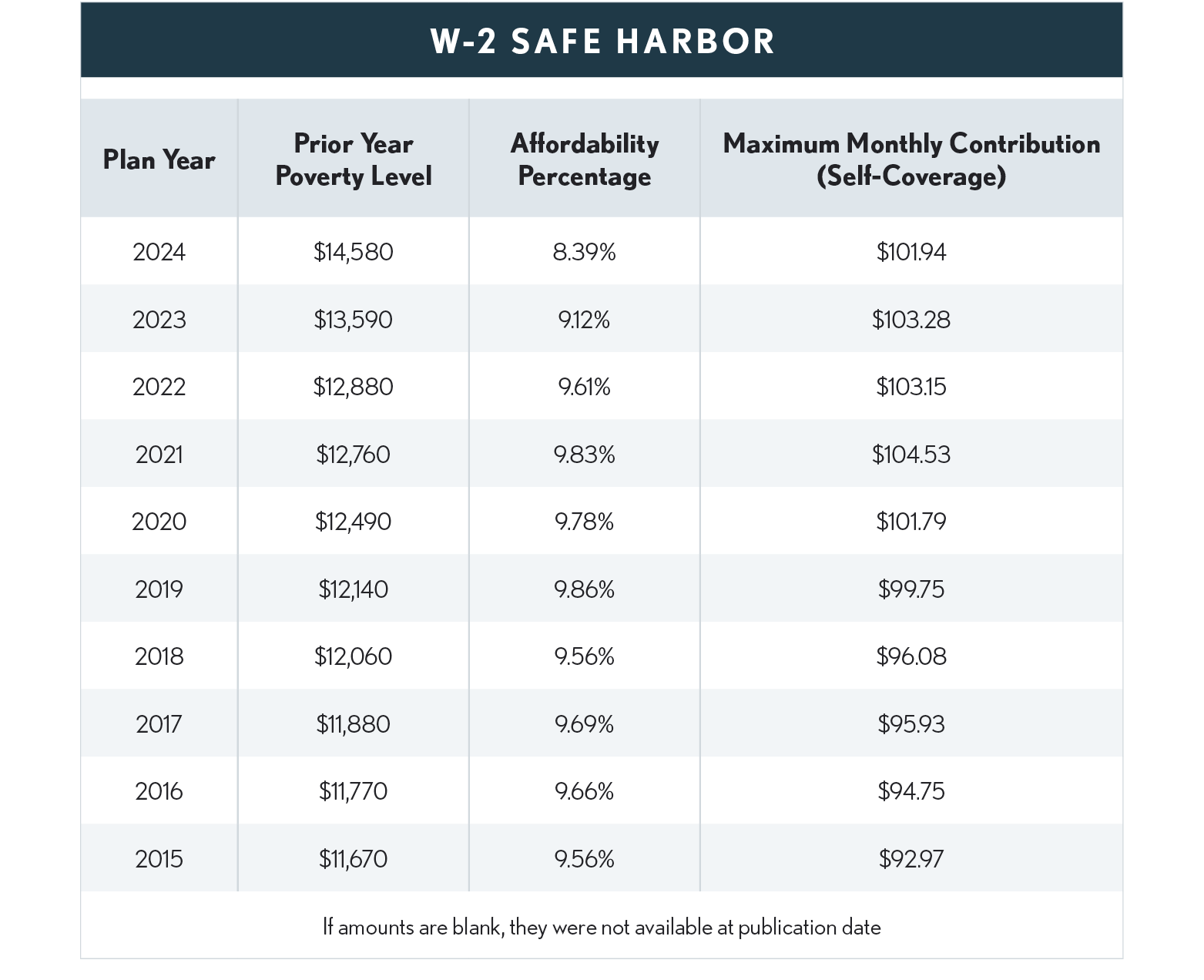

Form W-2 Safe Harbor (Post Year Safe Harbor)

• All Employees – The safe harbor is satisfied if the employee’s contribution toward the coverage for the calendar year does not exceed the affordability percentage (e.g., 9.12% for 2023) of Box 1 (wages) of the employee's Form W-2, Wage and Tax Statement, from the employer for the calendar year.