Moving Expense Reimbursement

Armed Forces members and other taxpayers before 2018 and after 2025 - Reimbursements to employees or self-employed individuals which aren’t for “qualified moving expenses” must be included in their gross income as compensation. A qualified moving expense reimbursement is one received for a deductible moving expense--such reimbursements do not have to be included in income. However, no deduction is allowed for any moving expenses for which non-taxable reimbursement is received.

Employer reimbursements for an employee’s moving expenses are treated as fringe benefits excludable from an employee’s gross income and wages if the:

-

Expenses would be deductible by the employee if he or she had directly paid or incurred the expenses; and

-

Employee did not deduct the expenses in a prior year.

Reimbursements should be made under rules like those relating to an accountable expense reimbursement plan.

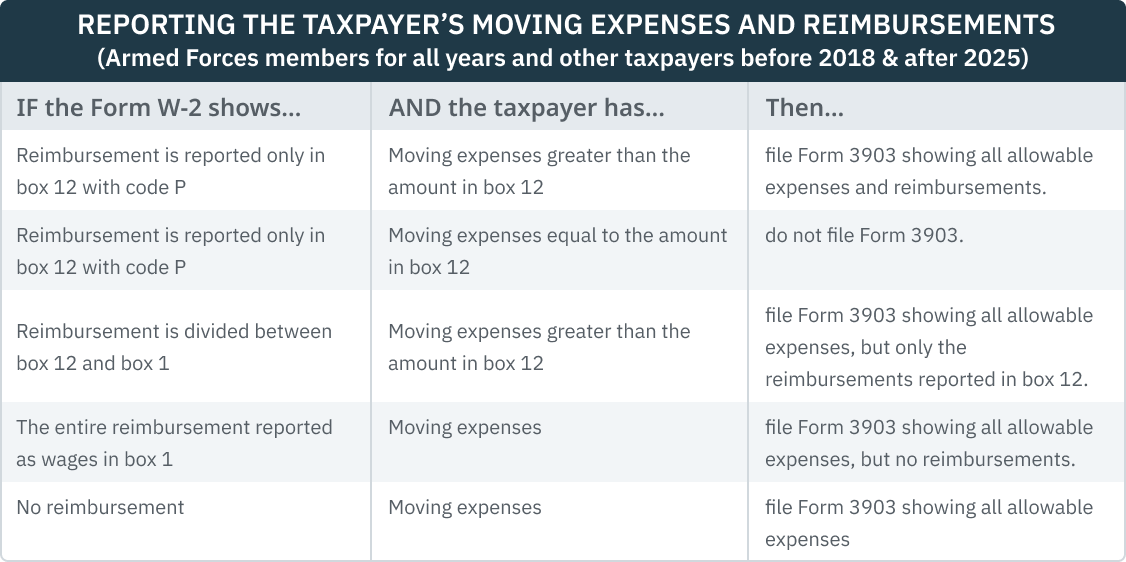

As far as W-2 reporting goes, reimbursements that qualify as excludable from income are not reported in Box 1 of the W-2; they must, however, be reported in Box 12 for informational purposes. They should be coded “P” to identify them as non-taxable reimbursements.

Taxpayers other than Armed Forces members for years 2018 through 2025 - Employer reimbursement of qualified moving expenses is no longer tax-free; the reimbursements will be treated as taxable income. (Sec 132(g)(2), as amended by TCJA)

Transitional Relief - The IRS has provided transitional relief for employee moving reimbursements received in 2018 for moving expenses incurred prior to 2018. These reimbursements continue be excluded from employee income and deductible as a fringe benefit by the employer. (IR 2018-190)